Report from the

{ Chief Financial Officer }

TIMOTHY P. SLOTTOW

I’m very pleased to report that the University of Michigan continues to be financially healthy, despite the difficult economic conditions facing the state and the nation. Our disciplined budget approach carefully balances the university’s need to remain competitive with a challenging economic environment.

Our 34,000 faculty and staff share an unyielding focus on the university’s core missions and are committed to finding innovative ways to control costs and manage resources more productively. As a result, we continue to have the resources to make strategic investments in the facilities, programs, and people that enable the institution to remain one of the best public research universities in the world.

Because of these collective efforts, the university continues to maintain the highest credit ratings from both Standard & Poor’s (AAA) and Moody’s Investor Services (Aaa). These ratings are important indicators of our strong financial health and outlook and are particularly encouraging in light of the tumultuous economy we’ve faced for several years. It is impressive that the university is one of only three public universities in the country to maintain these highest possible ratings.

In summary, the university’s total net assets (assets less liabilities) decreased by $2.1 billion in FY 2009 to $8.7 billion. This decrease is primarily the result of investment losses of $1.9 billion, mostly in the Long Term Portfolio, the investment pool for the university’s endowment, which was impacted by the global financial crisis. The university’s endowment spending rule, which is designed to insulate operations from volatility in the capital markets, cushioned the impact of the investment losses on the university’s operating budget and there was no decrease in the endowment distributions to support the university’s operations in FY 2009. At June 30, 2009, the endowment totaled $6.0 billion, down from $7.6 billion the year before. However, it is important to note that primarily due to generous new gifts from alumni and friends and transfers the size of the endowment decreased by only 21 percent despite net investment losses of 23 percent and a distribution of $244 million from the endowment to support operations. Despite the significant volatility of investment returns, the university’s long-term diversified investment strategy continues to provide predictable support for university operations as well as endowment growth over time as demonstrated by our five- and ten-year average annual investment results of 7 percent and 9 percent, respectively.

The university’s long-term investment strategy combined with aggressive cost containment, successful fund-raising, moderate tuition increases, and relentless protection and enhancement of the world-class quality of U-M’s research, teaching, and clinical care will pave the way for our future. In the following sections, I will discuss the important contributors to the university’s overall financial health to provide context to the accompanying financial statements.

REVENUE DIVERSIFICATION

Revenue diversification has long been an important strategy for the university to achieve financial stability in light of unpredictable economic cycles. In the 1960s, for example, almost 80 percent of the university’s general fund revenues came from state appropriations, compared to the projected 22 percent in the FY 2010 general fund budget. The current mix of revenue can be seen on the charts located above, which show the FY 2009 operating revenue sources with and without the Health System and other clinical activities.

THE GENERAL FUND OPERATING BUDGET CHALLENGE

Although state appropriations have declined significantly since FY 2002, support from the state of Michigan remains an integral part of the university’s strength. State appropriations have decreased $42 million, or 10 percent, from $416 million in FY 2002 to $374 million in FY 2009. In contrast, if appropriations had grown at the level of the Consumer Price Index, our state appropriations would have been $114 million higher in FY 2009. To put the state’s current support in perspective, it is useful to consider that in a stable economic environment, it would take an additional endowment of approximately $7 billion to generate a revenue stream that would equal the current level of support.

Moving forward, our budget continues to be a challenge. We need to balance our commitment to academic excellence and access against our ongoing cost containment efforts and the need to invest in our future, all against the backdrop of the state’s uncertain financial circumstances. In adopting the budget for FY 2010, we anticipated a state appropriation of $363 million, which reflects a 3 percent reduction from the amount we received in FY 2009. State appropriations for FY 2009 and FY 2010 are buffered by one-time federal stimulus support and we are planning for possible significant reductions in FY 2011 and FY 2012.

The university’s deans, directors, faculty, and staff have been focused and diligent in reducing and reallocating $22 million in recurring general fund expenditures from the Ann Arbor campus budget for the coming year. This is in addition to the $135 million of recurring cost reductions achieved in the general fund over the previous six years.

By focusing on innovative solutions and through ingenuity and hard work, we have been able to limit tuition increases. The approved Ann Arbor campus budget for FY 2010 includes a relatively moderate increase in tuition rates of 5.6 percent for both resident and nonresident undergraduates and most graduate programs. This budget also includes $118 million in centrally funded financial aid, the largest investment in financial aid in the university’s history. Within that, centrally awarded financial aid for undergraduates is increasing by nearly 12 percent, which will help preserve access for our most financially vulnerable undergraduate students. The approved Dearborn campus budget includes a 6.7 percent increase in undergraduate tuition, a 3 percent increase in graduate tuition, and a nearly 7 percent increase in institutional financial aid. At UM-Flint, the approved budget includes a 6.5 percent increase in undergraduate tuition, a 4.9 percent increase in graduate program tuition, and an 8.5 percent increase in institutional financial aid.

In FY 2010, many of our students will also see fewer loans and more grant aid in the form of more generous Pell Grants, increases in the American Opportunity Tax Credit, and more money for our work-study program. It is also noteworthy that the average rate of growth in our tuition during the past five years has been among the lowest of the public universities in the state of Michigan.

THE NORTH CAMPUS RESEARCH PROJECT

In June 2009, the university completed its purchase of the former Pfizer pharmaceutical research complex adjacent to the university’s current North Campus. This acquisition of 174 acres and 30 buildings was funded primarily with Health System resources and provides a springboard for new discoveries, job creation, and educational opportunities—an important investment for the university’s future. Known collectively as the North Campus Research Complex (NCRC), the nearly 2 million square feet of sophisticated laboratory facilities and administrative space acquired could expand the university’s research capacity by 10 percent.

This strategic purchase will save the university both time and money over the long term compared with the cost of building new research facilities. The NCRC is particularly beneficial for the university’s growing research activities in health, biomedical sciences, and other disciplines, which have been challenged in recent years by lack of research space. This investment also results in significant environmental benefits since the acquired buildings and their high-end research space will be preserved and utilized instead of demolished and transported to a landfill. The university will also use its multi-faceted environmental programs to benefit the NCRC.

OTHER PHYSICAL PLANT IMPROVEMENTS, SUSTAINABILITY, AND PRODUCTIVITY

It is important that we continue investing in our future by carefully choosing which facilities should be renovated or replaced. The institution’s facilities serve a wide range of needs, including everything from providing patient care to academic needs.

To support this effort, the university has invested an average of $396 million per year, over the past decade, for renovation and replacement of buildings and related infrastructure. FY 2009 was no exception as the university completed 286 projects across campus, an investment of $760 million. Many facilities to support the university’s academic, research, patient care, and athletic functions have recently been completed or are currently under construction to meet the university’s changing needs.

Two of the largest construction projects in university history are continuing with the North Quad Residential and Academic Complex, the university’s first new residence hall on the Ann Arbor campus in 40 years, and replacement of the C.S. Mott Children’s Hospital and Women’s Hospital facility. In FY 2009, completed projects include the Alumni Memorial Hall Museum of Art addition and renovation, the new Stephen M. Ross School of Business, a new student housing facility for the Flint campus, and the comprehensive renovation of Mosher-Jordan Residence Hall, which also includes the new Hill Dining Center.

The Athletic Department, through sound financial management and additional revenue sources such as those from the Big Ten Network and donor contributions, continues to make significant investments in its facilities. The renovation of Michigan Stadium, home to the football team since 1927, continues, with completion scheduled before the 2010 season begins. Construction is also continuing on the Al Glick Field House, a new indoor practice field for the football program, and a new 18,000-square-foot wrestling center is under construction.

The university is focused on improving usage of its instructional, research, and administrative space. Space utilization efforts include a change to centrally scheduled classrooms for all general fund buildings, targeted reporting on space and utility costs by building, and standards for office size and energy efficiency for all new and renovated buildings.

Planet Blue is a three-year, campus-wide effort to cut utility costs and increase recycling. The university spends more than $100 million a year on utilities and Planet Blue aims to cut those costs by 10 percent through a combined approach that includes energy-saving technologies, building upgrades, and engaging faculty, staff, and students in the program through an education and outreach program. Some of the energy-saving actions undertaken by the Planet Blue initiative include occupancy sensors for lighting, scheduling changes to heating and cooling systems, and modifications to water faucets in restrooms. Planet Blue is part of the campus-wide Energy and Environmental Initiative that was launched in 2007. The initiative’s annual report is available online at www.oseh.umich.edu/reporting.html.

Our cost containment and productivity improvement efforts to date have been paying off, thanks in part to leveraging technology and streamlining administrative processes. Over the past five years, the university’s general fund expenditure growth rate has been below the measure of inflation most appropriate for universities, the Higher Education Price Index (HEPI). The highest growth item during this time period among general fund expenditures has been scholarships and fellowships, reflecting our ongoing commitment to affordability and accessibility. And, the university’s general fund expenditures per student credit hour (net of the scholarships and fellowships the university provides) grew at an annual rate of 2.1 percent between FY 2003 and FY 2008, when the HEPI grew at an annual rate of 4.3 percent and the U.S. Consumer Price Index (CPI) grew at an annual rate of 3.1 percent.

Refer to Cost Containment for more information about the university’s increased productivity and strategic cost containment programs.

CONTROLLING HEALTH CARE COSTS

Organizations across the country continue to be challenged by escalating costs of employee and retiree benefits. Large employers report a lower rate of annual increase averaging about 8 percent over the past year, down from previous averages as high as 12 percent. Still, the cost growth is an ever-present challenge, with total university health care spending for employees and retirees reaching almost $283 million in FY 2009.

During the past fiscal year, the university drew upon the combined expertise of top clinical and health policy faculty and financial experts to design a new health benefits premium structure. Effective in January 2010, the new model will increase the overall contribution toward health care coverage made by employees, dependents, and retirees. A system of salary bands for active employees helps determine the contribution amount to lessen the impact on lower paid employees. Phased in over two years, these changes will provide a reduction in health care expenses of more than $31 million annually once fully implemented in 2011. Prevention, early intervention, and wellness also help to reduce the pressures on the health care system and promote overall control of costs.

The university’s health and wellness effort, known as MHealthy, addresses these important factors. MHealthy offers a spectrum of programs designed to support healthy lifestyles. During FY 2009, MHealthy completed the first university-wide health risk assessment, with more than 17,500 faculty and staff completing an online health risk questionnaire and participating in a wellness screening at sites located on all U-M campuses and in the U-M Health System. This new data gives the university a rich opportunity to understand our greatest community health risks in ways never before possible, and to use the data to design targeted programs and interventions that invest in health improvement and thereby reduce the costs incurred by the university’s health plans.

The university-managed prescription drug program continues to contribute to savings in the clinical realm, with a generic drug dispensing rate of just over 71 percent of prescriptions filled in FY 2009, up from 68 percent in the previous fiscal year and higher than the national average. Each 1 percent increase in the U-M rate of generic drug dispensing results in a savings of nearly $500,000 in reduced medication and co-pay costs.

THE ENDOWMENT

Our long-term diversified investment strategy is designed to maximize total return, while our spending rule policy is designed to protect and grow the endowment corpus in real terms and provide dependable support for operations. The financial market turmoil and large loss of wealth in global financial markets that followed the fall of Lehman Brothers in September 2008 exceeded any since the Great Depression. This resulted in broad-based losses across the university’s public and private equity and equity-like investments, with large losses occurring in areas that had experienced the greatest gains in recent years, such as real estate, energy, and other alternative investments. Despite the losses in FY 2009, these assets remain the university’s highest performing investments over longer time periods. Fixed income investments in the university’s long-term pool performed in line with expectations and proved to be a stabilizing factor on the overall investment portfolio.

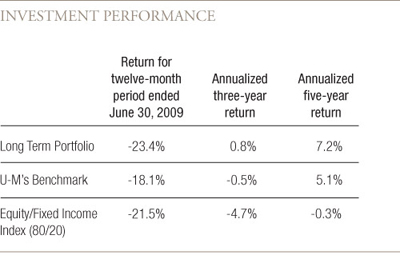

The Long Term Portfolio’s -23 percent return in FY 2009 follows a 6 percent return in FY 2008 and a 26 percent return in FY 2007. The Long Term Portfolio’s annualized five-year return of 7 percent was 2 percentage points above the custom market benchmark designed to capture the university’s long-term diversified investment strategy and nearly 8 percentage points over the undiversified benchmark consisting of major equity and fixed income indices in an 80/20 ratio. The return of the S&P 500 stock index was -2.2 percent over the same five year period.

The table above shows the endowment’s favorable investment performance relative to its benchmarks over longer time periods and its ability to support operations over the long term.

The university’s endowment spending rule smoothes the impact of volatile capital markets by providing for annual distributions of 5 percent of the moving average fair value of the endowment. Effective July 1, 2006, the moving average period was extended from three years to four years, and was extended by one quarter each subsequent quarter until it reached seven years at June 30, 2009. This change was enacted to further reduce distribution volatility, as well as to better preserve and grow the endowment corpus over time. The spending rule, along with the growth of the endowment, allowed for distributions to support operations of $244 million in FY 2009, for a total of $1.0 billion over the past five years.

The payout from our nearly 7,000 separate endowment funds enables us to serve a diverse population, ranging from patients in our Health System to students. For example, approximately $1.5 billion, or 24 percent, of our $6.0 billion endowment is restricted for use by our Health System, where nearly 1.8 million patient visits take place each year. The portion of the endowment available for university operations supports the education of more than 57,000 students. About 19 percent of our total endowment, or $1.15 billion, has been set aside for student aid, with nearly 80 percent of our undergraduate students who are Michigan residents receiving some form of financial aid, which includes grants, work-study, and loans. Endowment income also provides key support to the university’s research efforts, which have made countless contributions to our global society in areas ranging from medicine and law to the arts and sciences. The average effective annual spending rate from our endowment over the last 10 years, including spending rule payouts and withdrawals from funds functioning as endowment, primarily for strategic capital investment, was 6.5 percent.

THE HEALTH SYSTEM

The Health System, which integrates the clinical operations of the Hospitals and Health Centers, Medical and Nursing Schools, and Michigan Health Corporation under the direction of the university’s executive vice president for medical affairs, had a solid year financially despite the economic times, and continues to receive national recognition for its academic and clinical excellence. We take great pride in the fact that the Hospitals and Health Centers have experienced 13 years of positive financial margins, while also improving the quality and safety of the care we deliver to patients.

In FY 2009, the Hospitals and Health Centers achieved an operating margin of 1 percent ($18.5 million) on revenues of $1.8 billion. This smaller-than-expected margin reflects the strains of a difficult economy, an increase in patient care for those covered by government insurers, and a rise in uncompensated care provided to the uninsured and underinsured. That said, the continued achievement of a positive operating margin in this past year stands out from most other health care systems in the state and is a testament to the efforts of staff who work constantly to redesign operations for better efficiency and lower cost. The positive margin allows us to fund critical facilities and programs that will enhance patient care for a growing patient population, as well as research and education. These include the newly acquired North Campus Research Complex, the new C.S. Mott Children’s Hospital and Women’s Hospital, which will open in 2012, and the expansion of the Kellogg Eye Center and Brehm Diabetes Center, which will open in 2010.

Even within existing facilities, capital projects such as a new Observation Unit and new inpatient beds in existing areas of the University Hospital, and advanced medical imaging equipment, continue to expand our capacity to serve patients and ensure their safety. As we look to the future, the North Campus Research Complex presents a transforming opportunity to expand and align biomedical research capabilities at the Medical School and other areas of the university, and to consolidate administrative functions that currently occupy leased space outside our campus environment.

With the Medical School now among the top 10 in the nation in research funding from the National Institutes of Health, the timing for this purchase could not be better. Philanthropy directed toward the Health System continues to be very strong and supports our clinical, biomedical research, and medical education missions in many ways. In FY 2009, major gifts included a new $22 million gift from retail pioneer A. Alfred Taubman to further endow the institute he founded in FY 2008 with an original $22 million gift.

FINANCIAL CONTROLS

We are continuing our efforts to leverage best practices from the Sarbanes-Oxley Act through our annual financial stewardship and internal controls certification process, which is required for all deans and vice presidents at the institution. This year, we added cash handling and journal entry processes to the annual certification, which already includes other key risk areas such as information technology security, employment, purchasing card controls, and conflicts of interest. We are also providing a variety of tools and aids to units across campus such as web-based trend and exception reporting capabilities to help support management oversight. Beyond that, we developed written documentation templates to clearly define the key control points and procedures associated with our major financial-related processes.

CONCLUSION

It is, once again, satisfying to receive an unqualified opinion from the university’s independent financial auditors (PDF). This opinion signifies that the financial statements present fairly the financial position of the university. Included is my certification of management’s responsibility (PDF) for the preparation, integrity, and fair presentation of the university’s financial statements.

I encourage you to read Management’s Discussion and Analysis (PDF). It provides the details of the university’s financial strength, prudent financial policy, and most importantly, the capability and commitment to sustain the highest level of excellence in fulfilling the university’s mission for many decades to come.

Timothy P. Slottow | Executive Vice President and Chief Financial Officer